Resepi Fish Cake Homemade. Dijamin Bersih, Diyakini Halal, dan Dapat Makan Puas-Puas! Rupanya Senang Je Nak Buat…

__________________________________________________________________________________________

Top 9 Best Companies to Refinance and Consolidate Graduate Student Loans

Looking to refinance student loans? Want to consolidate student loans?

Today, the answer to that question is probably yes! 7 out of 10 graduates are now graduating with some form of student loan debt. With an average balance of $28,400, student debt is a big part of the average college graduate’s life.

At LendEDU, we help borrowers compare the top student loan companies in one place. We put together this guide to help you get information on all of the top student loan refinance lenders without having to jump around multiple websites. After you are done, you will know how to refinance and consolidate student loans.

Below we’ve ranked the leading student loan refinancing and consolidation companies. It is free to apply and the process usually takes about 15 minutes. How much could you save? Find out today. You might be able to save $20,000 or more!

Top Lenders to Refinance & Consolidate Student Loans With

You may now have a general idea of how to refinance student loans and how to consolidate student loans, as well as the basics of what each lender offers, but there is much more information you should know before choosing a lender. There are many different benefits and drawbacks of what each student loan consolidation and refinancing lender offers, and it is important to be aware of all of them. You will find all of the necessary information below.

Before you start an application, you should know that most lenders require a minimum FICO credit score of 660, 40% maximum monthly debt-to-income, and $24,000 in yearly gross income. If the requirements above sound good, we think that you are a great applicant for student loan refinancing and consolidation. Each lender has its own specific underwriting criteria, so you may have a higher chance of approval at certain lenders. Read the detail lender reviews for more information regarding lender approval. We hope after you are done you can make the best choice to refinance your student debt with.

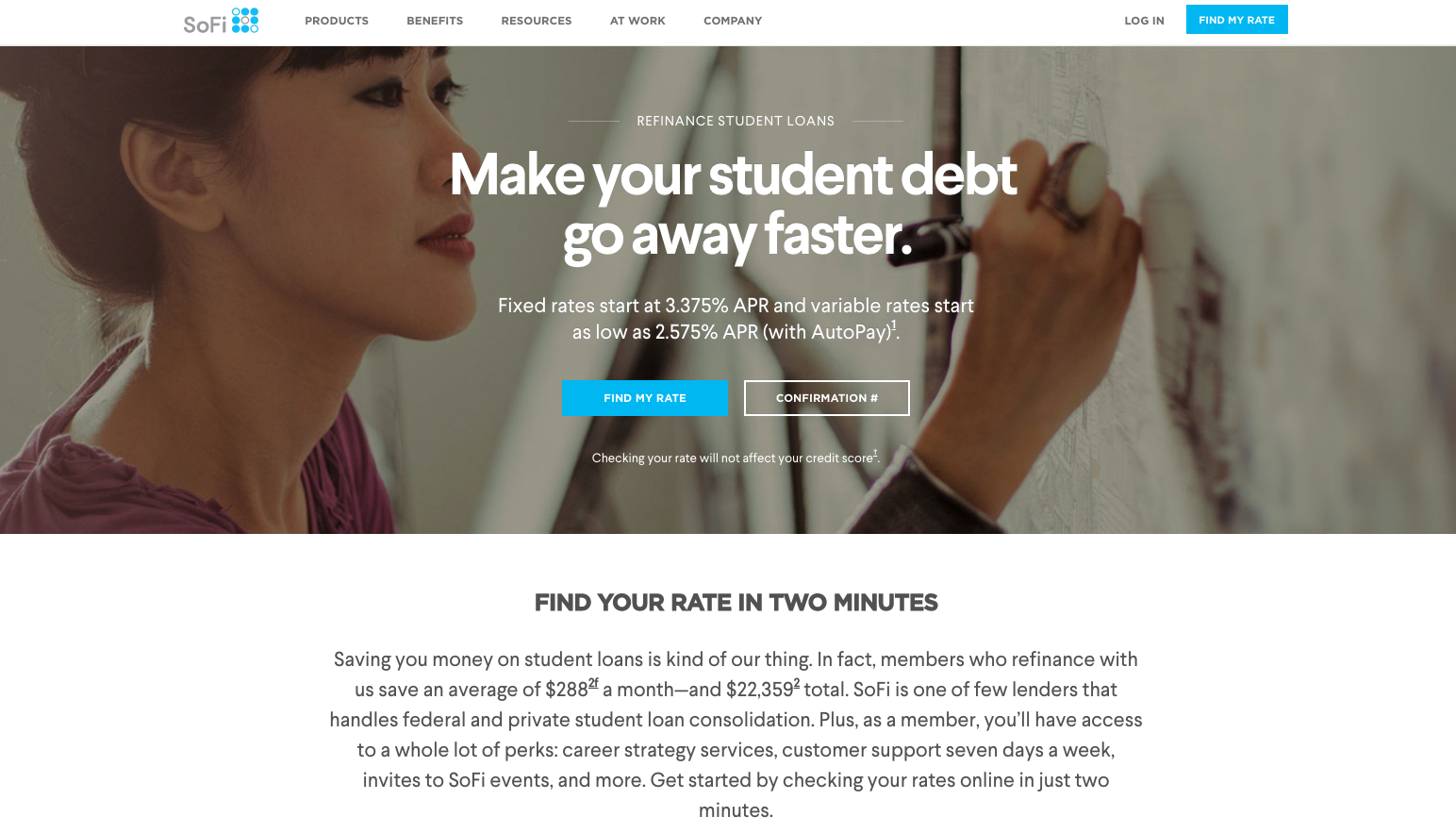

1. SoFi Review

Student loan refinance is a hot topic these days. Today, there are a number of new private consolidation companies looking to help borrowers improve their financial health. Our favorite, SoFi, aka Social Finance, has quickly positioned itself as the top student debt refinance lender on the market. SoFi was founded by a group of Stanford business students who wanted to help their peers escape from student debt with lower interest rates. The program launched at Stanford in 2011 and has quickly grown. Today, SoFi has expanded and now helps student debt borrowers to refinance student loans nationwide.

The Basics

SoFi offers borrowers both refinancing and consolidation services. Borrowers can select the loans they would like to refinance or consolidate, SoFi pays them off, and then borrowers pay off a new loan issued from SoFi. SoFi aims to help undergraduate and graduate borrowers lower their monthly payments and obtain lower interest rates. The company offers an interest rate discount of 25 basis points (0.25%) if you sign up for auto-pay. Signing up for auto-pay is easy and SoFi’s customer service support staff can help you through the process if you run into any trouble.

SoFi offers borrowers a number of great options. SoFi offers both variable and fixed interest rate loans. Borrowers can select from 5, 7, 10, 15, and 20 year repayment plans. The fixed rates start at 3.35% and have a maximum possible rate of 6.74%. The variable rates range from 2.79% to 6.72% and are tied to the LIBOR rate. If interest rates do happen to rise, variable interest rates will be capped at 8.95% to 9.95% APR. There are no penalties for paying off your debt early but borrowers are expected to make payments on a monthly basis.

SoFi Benefits

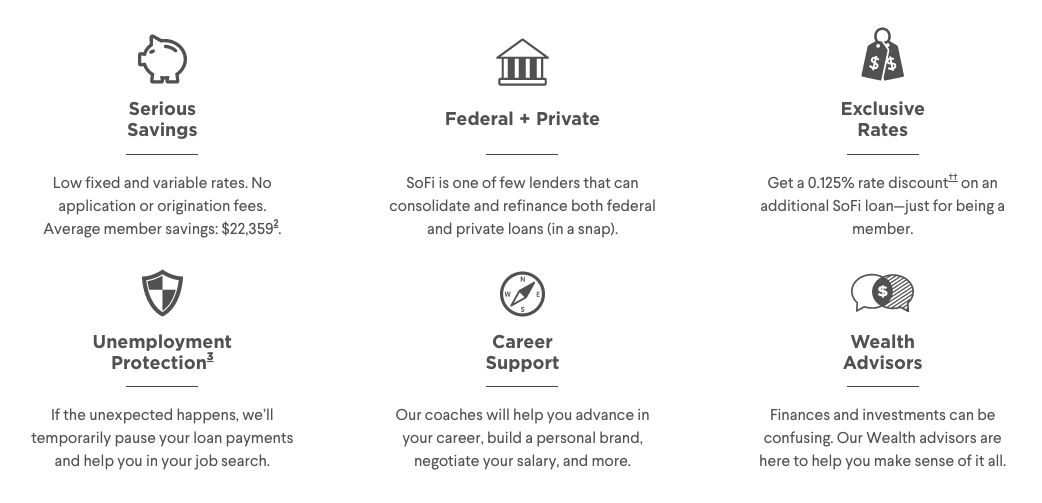

SoFi doesn’t charge origination fees when you refinance student loans through them. Origination fees are fees charged to borrowers for taking out a loan. These extra costs are usually added to the principal balance. SoFi has zero prepayment penalties, as well. At any time you can pay off your debt early. Whether you are looking to pay $100 extra each month, or are using that year end bonus to make an extra payment, you can be sure that you won’t be charged any fees for paying early.

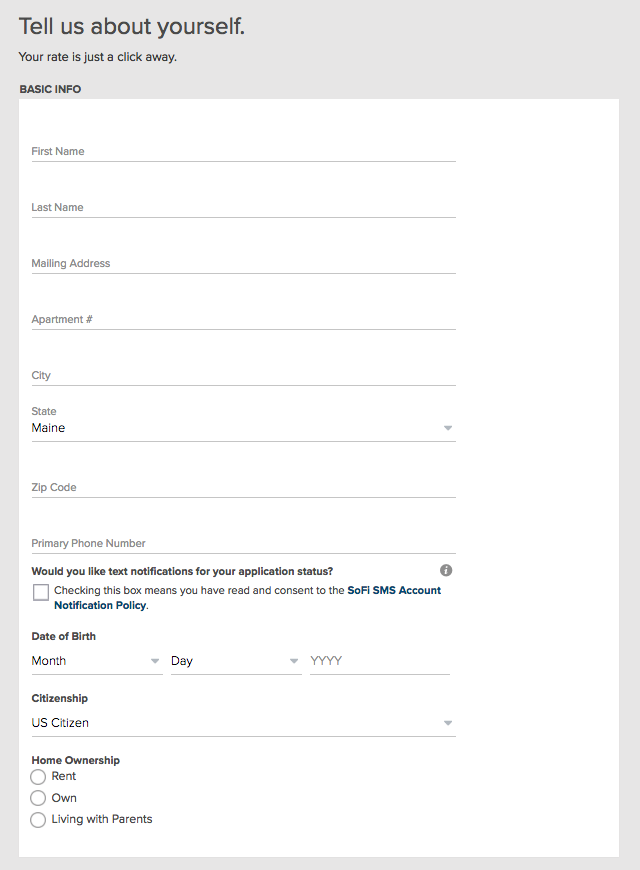

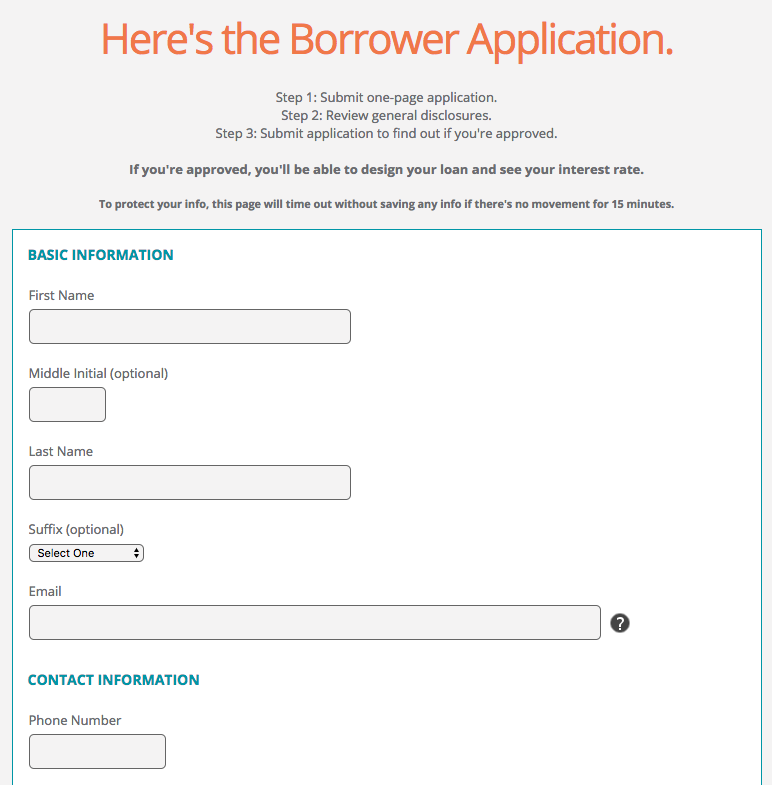

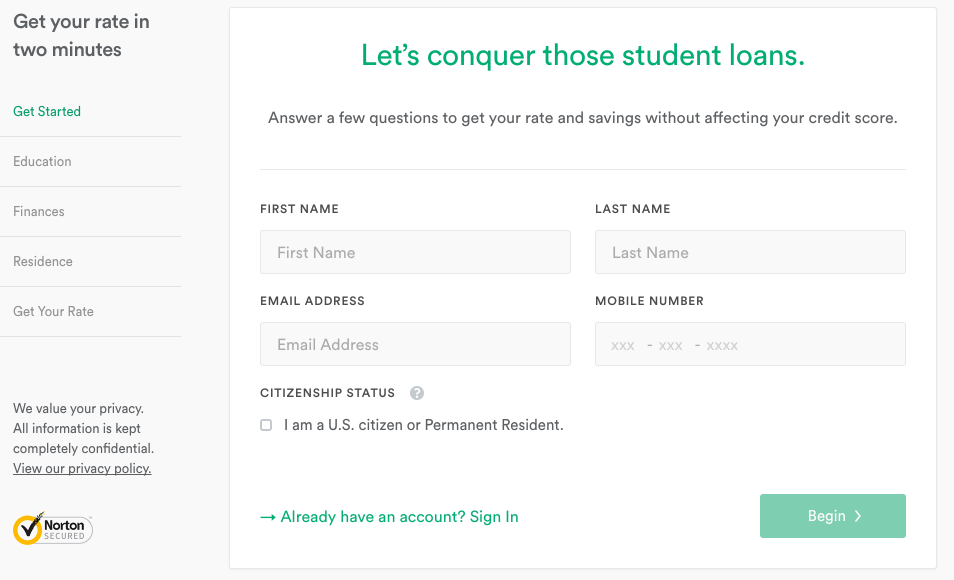

SoFi makes refinancing student loans simple. The company claims that it only takes 15 minutes to start saving.

Fill out a quick application, see if you’re approved, and refinance – simple as that! SoFi even makes it super easy to figure out how to consolidate students loans into one, refinanced loan.

See the image to the right to see what SoFi’s application looks like. It is very simple and straightforward, and can be completed in just a few minutes!

SoFi has a unique and proprietary approach to underwriting and the company takes a number of dimensions into consideration including alma mater, professional success, and income.

Also, SoFi has awesome customer service!

If you run into any problems along the way give them a call. Unlike the big old banks, SoFi understands that customer service is an important piece of the equation.

You’re in great hands with SoFi!

To Consider

SoFi is looking for well educated professionals with good income. Like most other lenders who refinance student debt, you should have good credit and a strong repayment history. SoFi primarily focuses on prime and super-prime borrowers, with an average borrower FICO score of 780 and income of approximately $150,000. The SoFi student loan refinance and consolidation program is a great option for people who want:

- Low interest rate options

- Term length options

- Great customer service

- Quick application process

Bottom Line

At LendEDU, we give SoFi our stamp of approval for refinancing your student debt. To get started you can start the application at SoFi!

- Refinance & consolidate both federal & private student loans

- Must have completed an eligible undergraduate or graduate degree program

- Undergraduate & graduate student loans are both eligible

- 5, 7, 10, 15, 20 year repayment terms

- 2.79% APR to 6.72% APR (with autopay) variable rates, capped at 8.95% to 9.95% APR

- 3.35% APR to 6.74% APR (with autopay) fixed rates

- Auto-pay discount

- Strong credit score, salary, and debt-to-income requirements

- Zero prepayment penalties

- Zero origination fees

- Unemployment protection – payments are temporarily suspended

- Career support for SoFi members

- Entrepreneur program

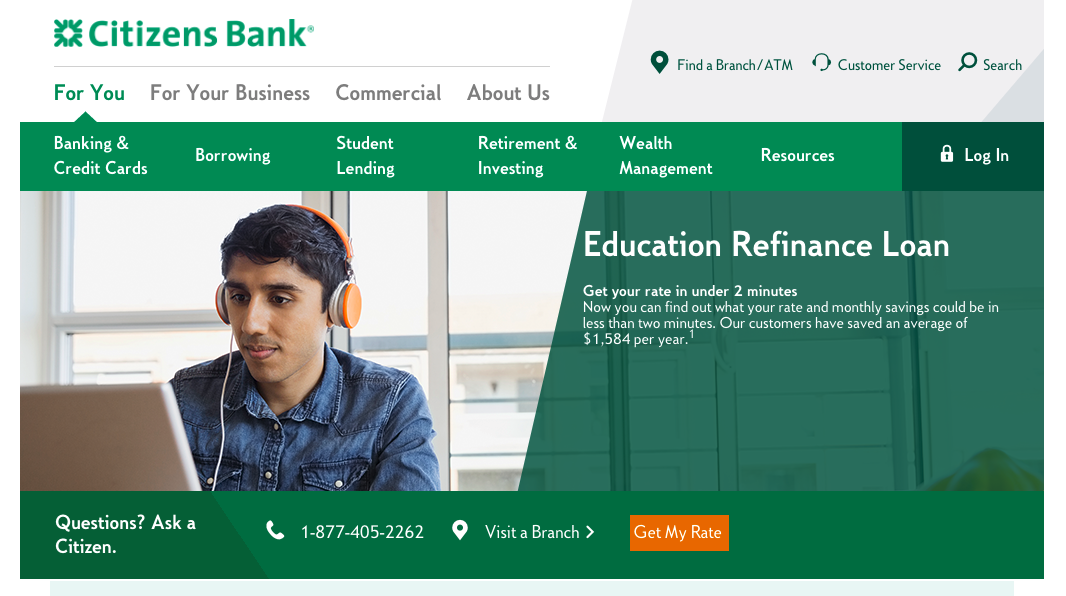

2. Citizens Bank Review

Navigating through the seemingly countless number of options for refinancing and consolidating your student loans can often be a daunting task. This is why we at LendEDU are trying to help borrowers navigate through the options to choose the one that will save them the most money. Citizens Bank is one of the most well-known companies that refinances student loans – and they are also one of the best. As the 13th largest retail bank with over $130 billion in assets and 1,200 branches, Citizens Bank offers many unique options and benefits for those looking to save money on their student debt. If you are one of these people, it would be in your best interest to strongly consider Citizens Bank. They make it easy to figure out how to refinance and consolidate student loans.

The Basics

Citizens Bank offers a variety of attractive options for customers. To start, the company offers both variable and fixed interest rates. Variable rates start at 2.78% while fixed rates may be as low as 3.74% – some of the lowest in the industry. Fixed rates stay the same over the life of the loan but variable rates fluctuate according to the LIBOR. Citizens Bank also offers repayment plans of 5, 10, 15, and 20 years. The minimum amount to refinance is $10,000.

As with SoFi, Citizens Bank charges no application, origination, or prepayment fees, and borrowers can save 0.25% on their interest if they sign up for auto-pay. Like many of the other lenders, borrowers can refinance and consolidate their student loans in order to reduce their interest rates or monthly payments.

If you end up choosing Citizens Bank, they will pay off whichever of your student loans you choose and issue you a new one. This will either save you money over the life of your loan or make your monthly payment more manageable, depending on the repayment term that you choose. On average, Citizens Bank customers save $1,584 per year!

Citizens Bank Benefits

As mentioned above, there are no fees associated with refinancing and consolidating through Citizens Bank. This means that you can apply for free and, if approved, you will not be charged for accepting the company’s offer. Finally, if you happen to have some extra cash to put towards your student debt, you will not be penalized for making extra payments.

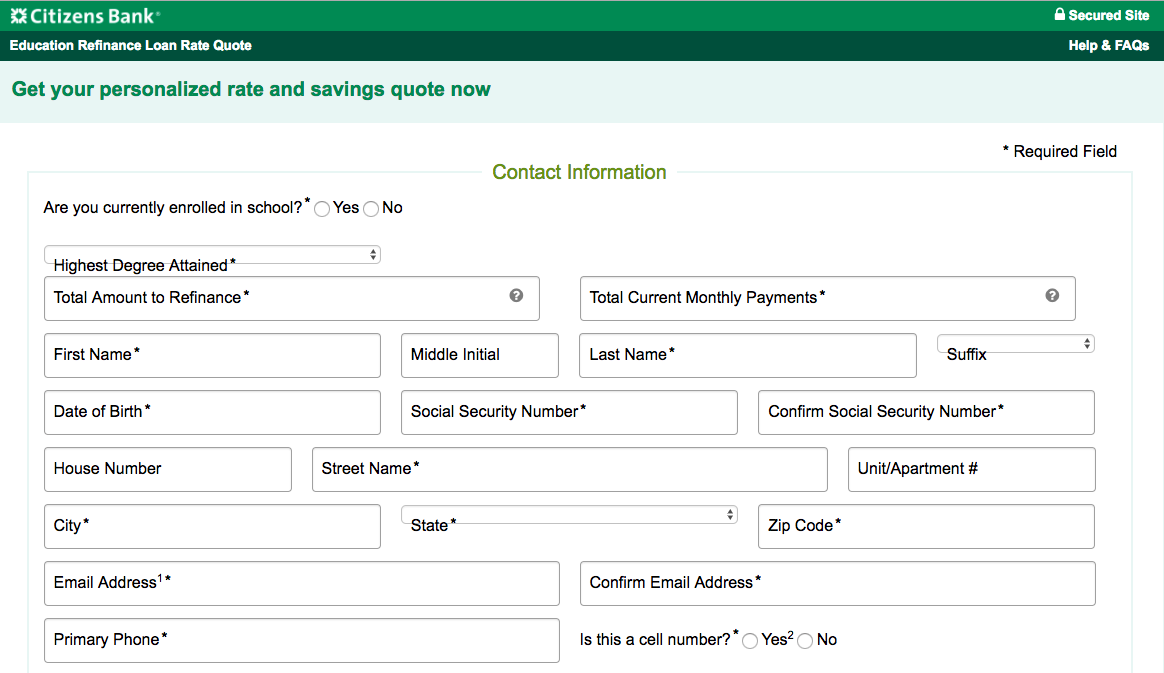

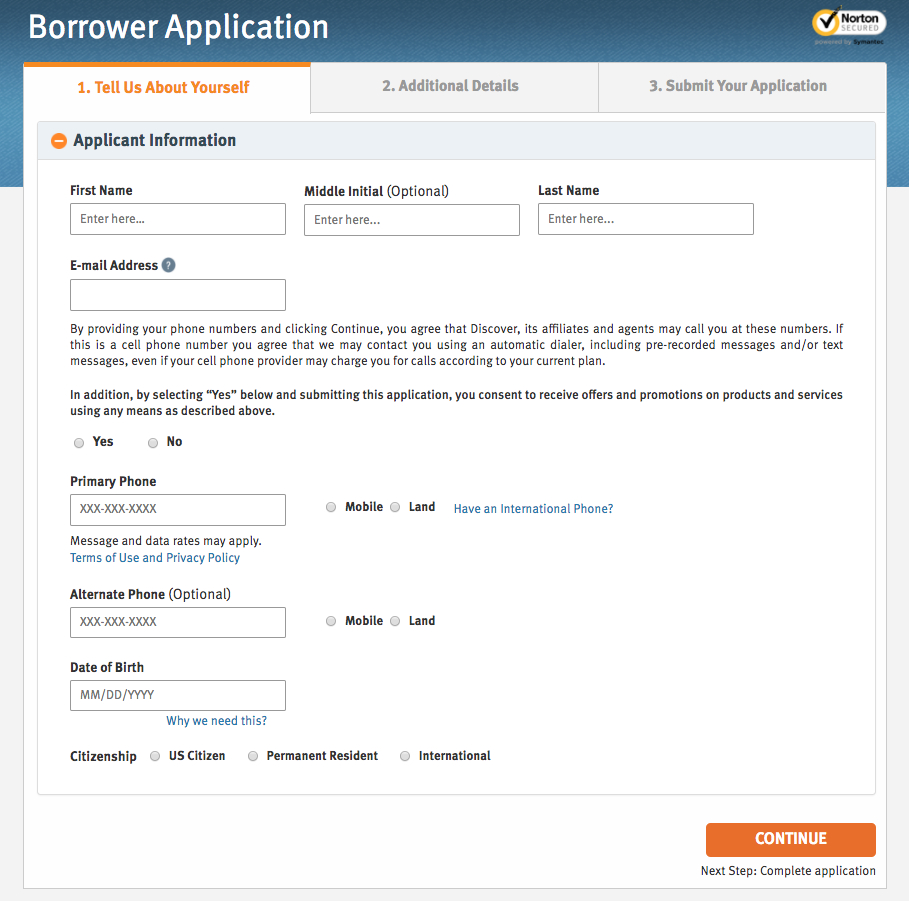

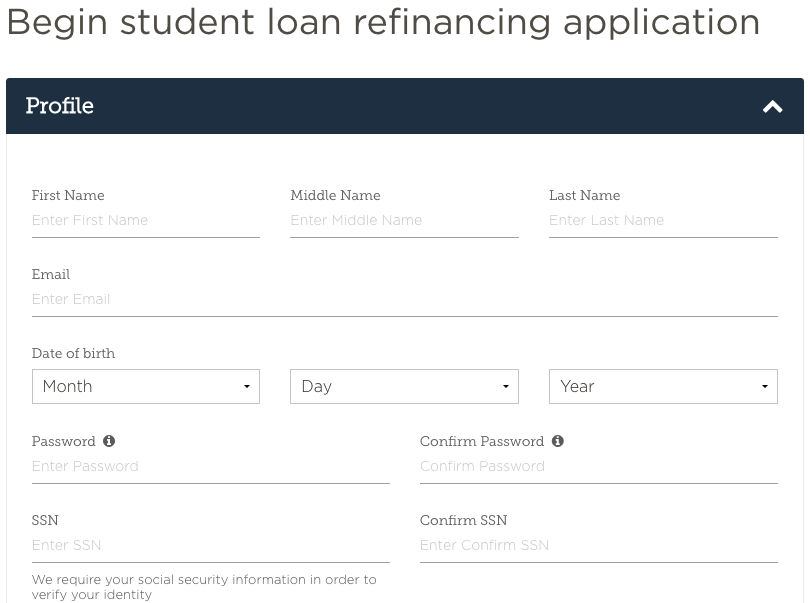

If you are interested in working with Citizens Bank, you can apply on the company’s website in about 15 minutes. The process if fairly straightforward and easy to do. Once you apply, Citizens Bank will run an initial credit check to determine if you may be eligible. If you meet the initial requirements, you will be asked to upload certain documents that help Citizens Bank’s underwriting team determine if you actually qualify.

Below you can see an image of what Citizen Bank’s application looks like.

One of the greatest things about Citizens Bank is its 24/7 customer service. The company has people standing by to help you at any point along the process, whether you are just applying to refinance or already have.

Citizens Bank also offers some great resources to help borrowers manage their debt. On the Student Services section of the website, there is an Education Refinance Loan Calculator, a College Savings Goal Calculator, and even a calendar to track payments.

To Consider

Though Citizens Bank offers competitive rates, some other companies have lower minimum rates. This, however, does not mean that you will automatically receive a lower rate elsewhere. Each lender has its own eligibility criteria and you may actually receive your lowest rate at Citizens Bank.

Bottom Line

The Citizens Bank student loan consolidation and refinance program is one of the best options for people who want:

- A wide variety of term length options

- A lower interest rate

- Unparalleled customer service

- A quick and easy application process

Here at LendEDU, we give Citizens Bank our highest recommendation. To get started, apply at Citizens Bank today!

- Refinance & consolidate both federal & private student debt

- Must no longer be in school

- 5, 10, 15, and 20 year repayment plans

- 2.78% APR (with autopay) for variable interest rates

- 3.74% APR (with autopay) for fixed interest rates

- Must have a strong credit score, secure job, low debt-to-income

- Zero application, origination, or prepayment fees

- 24/7 customer service

- See Citizens Bank DisclosuresŦ

3. LendKey Review

Finding the best refinancing or private consolidation company can be tough. Each lender has its own set of criteria, interest rates, and term lengths. Moreover, each lender brings something unique for borrowers. Cosigner requirements, credit score minimums, and customer service can vary at each lender.

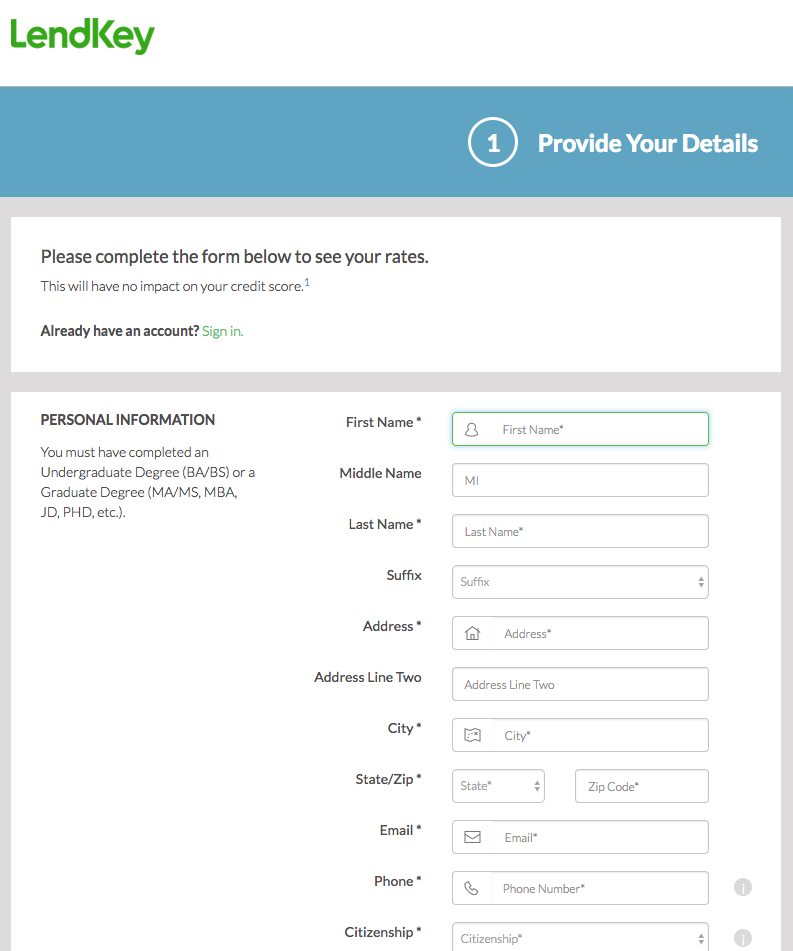

At LendEDU we work with only the top companies who refinance and consolidate student loans. One company trying to help borrowers is LendKey. At the end of the day, LendKey brings local credit unions to the table for borrowers. The result is great customer service and interest rate options for borrowers looking to save.

The Basics

LendKey is more than just a single company. LendKey is a collection of not-for-profit credit unions and community banks from across the U.S.A. The participating lenders work together to compete against major lenders.

The result is great interest rates for borrowers. And, with over 320 credit unions participating in the program you can be sure that there is an option available for you! There are also no geographical requirements.

The lowest interest rate that LendKey currently offers is 2.57% at a variable rate. Fixed rates, alternatively, start at 3.15%.

The company also requires a yearly income of over $24,000. Today, the company allows borrowers to refinance and consolidate both federal and private debt.

LendKey charges NO origination fees which can help borrowers save money. Moreover, cosigner release is an option after 12 months.

As far as credit criteria goes, LendKey requires borrowers to have a decent credit score and an average debt-to-income. LendKey has good approval ratings, so definitely apply, even if you are on the fence. We found that many of our users were approved at LendKey as the company evaluates each borrower on a case-by-case basis.

LendKey offers term lengths of 5, 7, 10, 15 and 20 years. There is no penalty for paying off debt early, and borrowers can have up to four years of interest only payments. Borrowers are expected to make payments on a monthly basis. The company offers an interest rate discount of 25 basis points if you sign up for auto-pay.

The first part of the application should only take a few minutes to complete. If approved, applicants are expected to join the local credit union that will be providing the financing. Credit unions usually require a small deposit for membership. In most cases borrowers will need to deposit $1 to $20 to gain access to the credit union. A $5 deposit is a small price to pay for great customer service and interest rates. Don’t worry, the LendKey representatives can help you if you run into any trouble along the way!

LendKey Consolidation Benefits

LendKey offers borrowers a personal experience. Borrowers will receive a friendly credit union experience as compared to the typical treatment from a big bank. Credit unions operate for their members (you!) and only the members. All earnings are redistributed back to the members so you can be sure that every lender on the LendKey platform has your back. The company doesn’t have any shareholders or investors so they can focus all of their attention on you!

LendKey has zero origination fees! Origination fees are fees charged to borrowers for taking out a loan. These extra costs are usually added to the principal. But with LendKey you can avoid these costs all together. By not having an origination fees, LendKey makes it easy to compare the value of a consolidated loans against the current loans that borrowers already have.

LendKey has zero prepayment penalties, as well. For people working to pay off their student debt early, zero prepayment penalties are important. Some lenders charge borrowers when they pay off their debt early. LendKey puts the borrowers first and will never charge you if you pay off your debt early; so if you come into that year end bonus, you don’t need to fear paying off your obligations early.

Another great benefit of LendKey is cosigner release. This means cosigners can be released from the debt after 12 months of on-time payments! This is a big deal. Not many lenders offer cosigner release. This one year release is by far the shortest release on the market. With cosigner release you can positively influence your cosigner’s credit score too.

To Consider

The major disadvantage is that LendKey is a newcomer in the student loan consolidation market.

Bottom Line

The LendKey refinancing and debt consolidation program is a great option for people who want:

- Cosigner release after 12 months of on-time payments

- Low interest rates

- A personal approach to borrowing

- Great customer service

- A credit union experience

More Details

- Must have completed an eligible undergraduate or graduate degree program

- Undergraduate & graduate student loans are eligible

- Consolidate student loans together (both federal & private)

- Variable rates as low as 3.15% (with autopay)

- Fixed rates as low as 2.57% (with autopay)

- Interest only repayment option

- 5, 7, 10, 15, and 20 year repayment terms

- No origination fees or prepayment penalties

- Medium credit score, salary, and debt-to-income requirements

- Not-for-profit lenders

- Excellent customer service

- Cosigner release available, if, the primary borrower is eligible even without a cosigner.

4. ELFI Review

In 2015, SouthEast Bank of Tennessee launched its student loan refinancing and consolidation program to borrowers through ELFI, Education Loan Finance. Although the ELFI program is a newcomer to the refinancing scene, its management has over 30 years of experience in the student lending industry, and customer testimonials indicate that their expertise in the subject helps borrowers in choosing the right loan program for their financial goals.

The Basics

ELFI offers very competitive interest rates to approved borrowers. If approved, ELFI will pay off your old loan(s) and give you a new, single loan with a new interest rate and/or loan repayment term. ELFI offers student loan refinancing and consolidation to both recent graduates as well as parents with Parent PLUS and private student loans.

You can find out if you are eligible for refinancing with ELFI by applying on the company’s site. To get an idea of what the application looks like, see the image to the right.

ELFI offers variable interest rates ranging from 2.49% to 6.01%. Alternatively, approved borrowers may opt for a fixed interest rate ranging from 3.19% to 6.69%. ELFI offers low rates even without the automatic payment discount that many lenders offer.

The minimum amount to refinance is $15,000 while the maximum is based on the borrowers qualifications.

ELFI offers repayment terms of 5, 7, 10, 15, and 20 years for recent graduates. This wide range of options can help all kinds of borrowers. Those with high income may opt for a shorter repayment term, saving them money over time. Those who want lower monthly payments, on the other hand, can choose a longer repayment term. For parents, ELFI offers repayment terms of 5, 7, and 10 years.

ELFI Benefits

Aside from helping borrowers lower their interest rates and make their repayment more manageable, ELFI offers some enticing benefits.

First off, ELFI offers cosigner release of existing education loans to approved borrowers who qualify for refinancing based on their own credit and financial profiles. This removes cosigners from the original loans, relieving them of future payment responsibilities and potentially helping them improve their credit.

Another great benefit of ELFI is its Fast Track Bonus. If approved borrowers accept their offers from ELFI and submit all the required paperwork within 30 days of the initial application date, they can receive $100. This can be a great way to earn some extra money to put towards that pesky student debt!

To Consider

Though ELFI displays some of the lowest rates in the industry, it does not necessarily mean you will receive a lower rate with them as compared to other lenders. Each lender has a different eligibility criteria and underwriting process so your offered rates (if approved) may be higher than those from other lenders.

Bottom Line

ELFI is a student loan refinancing lender with low interest rates and a variety of repayment terms. To see if you are approved for refinancing with ELFI, start your application on the company’s website!

- Refinance and consolidate both federal and private student debt

- Must have an eligible degree from an approved post-secondary institution

- Variable rates ranging from 2.49% – 6.01%

- Fixed rates ranging from 3.19% – 6.69%

- Repayment terms of 5, 7, 10, 15, and 20 years

- Refinancing of Parent PLUS loans available in 5, 7, and 10 year terms

- $100 bonus for completing required paperwork within 30 days of application

- No application, origination, or prepayment fees

5. CommonBond Refinancing Review

So you just graduated from a great school and you’re stuck with a mountain of student debt. Welcome to the club. In 2012, a few students from the University of Pennsylvania found themselves in this situation and sought out to help borrowers like themselves.

These MBA students were tired of high interest rates on their student loans and sought out to change the industry. They founded CommonBond.

Today, CommonBond has raised over $100 million in funding with the goal of making student debt more affordable through refinancing and consolidation. The company now serves over 700 graduate programs across the U.S. CommonBond makes it easy to figure out how to refinance student loans and how to consolidate student loans.

The Basics

CommonBond allows borrowers to consolidate and refinance both federal and private student loans. The company offers borrowers an array of options to consider including 5, 7, 10, 15, and 20 year terms with both variable, hybrid, and fixed interest rate options.

The range of interest rates for Common Bond start as low as 2.79% for its 5-year variable rate product and start at 3.35% for its fixed rate product.

Like most lenders lenders, CommonBond does not charge an origination fee and there is no pre-payment penalty for paying off your debt early. At this time borrowers can apply to consolidate up to $500,000 in student debt.

CommonBond works with anyone with a minimum of a 4-year undergraduate degree from over 2,100 schools nationwide, as well as those with grad school debt. In addition, they work with parents who took out PLUS loans for their children’s education.

CommonBond Benefits

CommonBond offers some of the lowest student loan refinance and consolidation interest rates on the market. Without origination fees and prepayment penalties, it is easy for borrowers to compare CommonBond alongside their current loans.

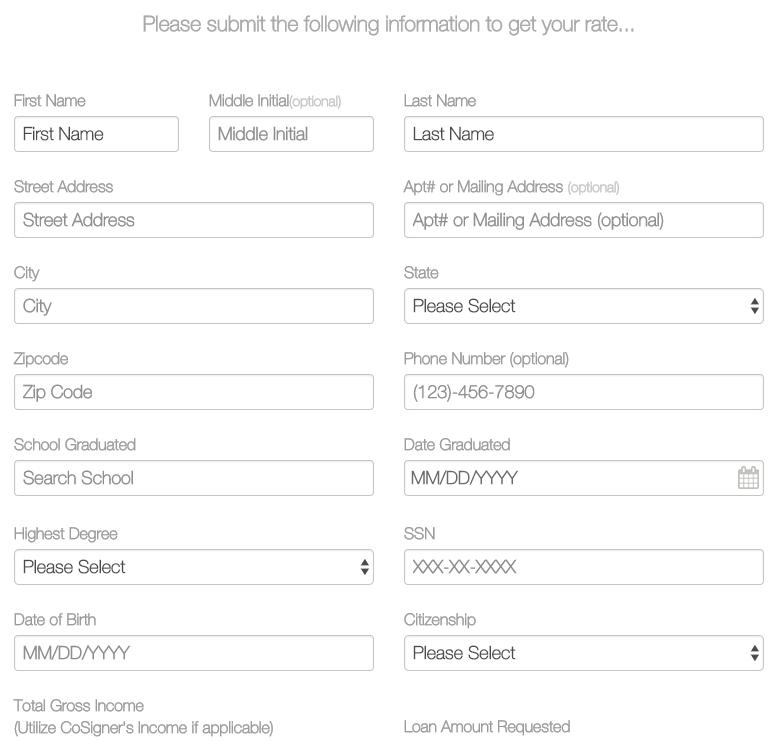

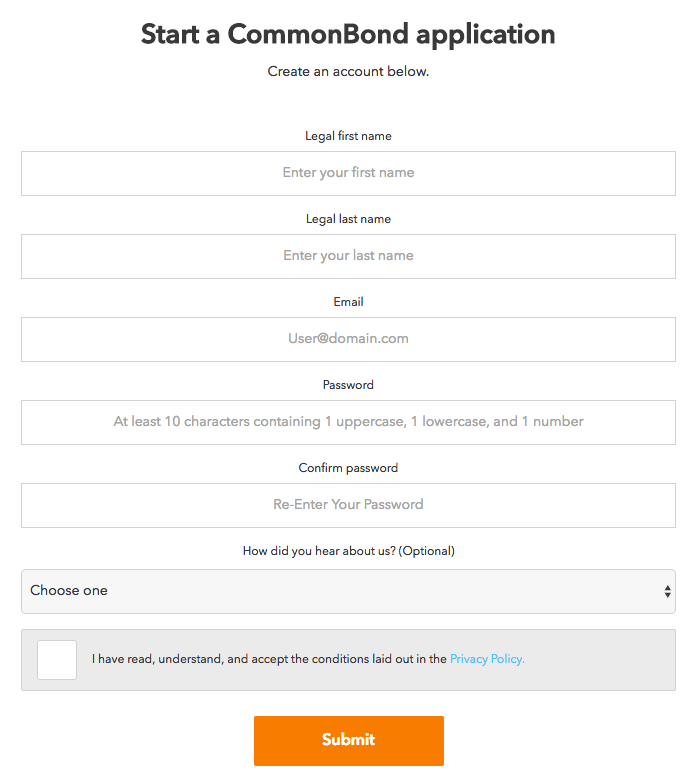

Additionally, CommonBond has a smooth and easy application process. After creating an account and entering some basic background information, as well as information about your student loans, you will be able to see if you may qualify. To get an idea of what the app looks like, see the image to the right.

Out of all the refinance lenders we work with, CommonBond has some of the best customer service. The company prides itself on helping it borrowers navigate the refinance market and beyond. The company even has a program to help borrowers who lose their jobs find a new one.

CommonBond is building an incredible reputation for itself and clearly cares about its borrowers unlike any other company we’ve seen.

To Consider

In general, CommonBond looks for applicants with very strong income. To be approved by CommonBond you must have good credit, a well paying job, and be able to afford your monthly payments.

Bottom Line

The CommonBond student loan refinance and consolidation program is a great option for people who want:

- To lower their monthly payments

- Lock in low interest rates

- Choose from a variety of term lengths

- Consolidate student loans together (both federal & private)

At LendEDU, we give CommonBond our stamp of approval. To get started you can start the application at CommonBond!

- Refinancing & consolidation for private & federal debt

- Must have a Bachelor’s degree from any of the over 2,100 schools that comprise the CommonBond school network

- 2.79% – 6.01% APR variable rate financing (with autopay)

- 3.35% – 6.74% APR fixed rate financing (with autopay)

- 5, 7, 10, 15, and 20 Year Repayment Terms

- 0.25% interest rate discount with auto-pay from a checking account

- Moderate credit score, salary, debt-to-income and other criteria

- Unemployment protection – payments are paused temporarily

- Access to CommonBond Community including networking events and other perks

6. College Ave Student Loans Review

College Ave Student Loans is a leading provider of refinancing and consolidation. Founded in 2015, College Ave is leading the way with low interest rates and the fastest turnaround time in the industry. Continue reading to learn more about College Ave’s student loan refinancing product.

The Basics

Aside from flexibility, College Ave Student Loans makes the application process simple and easy.

Applications are quick and to the point with no additional hidden fees throughout the process. The College Ave application process only takes 3 minutes. Most other applications take 30 minutes to complete. College Ave also really makes it easy to figure out how to consolidate multiple student loans into one!

You can see what the beginning of the application looks like to the right. As you can see, it is very clean and easy to use. College Ave has one of the most user-friendly applications of all the lenders!

There are two types of interest rates available to choose from: fixed and variable. Variable interest rates fall within a range of 4.13% to 7.13% APR while fixed interest rates vary between 4.65% and 7.50% APR. Keep in mind, these rates include the interest rate discount of 0.25% for making automatic debit payments.

Multiple repayment terms are available to borrowers who want to refinance student debt. The lowest term to choose from is five years; on the contrary, the longest repayment term is up to fifteen years. Different payment lengths can be chosen so long as they fall within the range that is specified.

After refinancing is completed, borrowers may choose between two different repayment options. Individuals have the option to make full principal and interest payments immediately after disbursement. If this is too much too soon, customers have the option to defer principal payments for two years while making interest payments.

There are no application or origination fees when refinancing and consolidating with College Ave. The process to apply is quick and easy – one of the best parts of College Ave’s program.

College Ave Benefits

College Ave offers multiple repayment terms with a wide range of interest rates.

Whether you are looking for a fixed rate, a variable rate, or an interest-only repayment plan, there are plenty of options to consider. College Ave is one of the only companies to offer an interest-only payment option for 24 months.

One of the best benefits offered by College Ave is a 0.25% interest rate deduction with auto-pay. This interest discount is applied for setting up automatic payments.

Keep in mind that every interest rate stated in this article is after the application of this discount.

To Consider

Any borrower who is approved can consolidate student loans through College Ave. It is a newer company, so there are less reviews out there, but we do highly recommend College Ave to any borrowers who want to refinance.

Bottom Line

College Ave is a great choice for undergraduates, graduates, and parents interested in:

- Low interest rates

- Flexible payment term options

- An easy application process

More Details

- Fast application process

- Variable Interest rates: 4.13% – 7.13% APR (with discount)

- Fixed Interest Rates: 4.65% – 7.50% APR (with discount)

- Payment terms ranging from 5 to 15 years

- Two different payment options

- Full principal and interest payments made immediately

- Interest only payments for two years

- $0 in application and origination fees

- Minimum: $5000

7. Discover Student Loans Consolidation Review

With the cost of going to college increasing, many students are taking out both federal and private student loans in order to help fund their degrees. When they graduate and start working, they then find that they’re paying more than they need to for their student loans and look at refinance and consolidation options. Discover Student Loans offers consolidation loans that are made by Discover Bank and are an affordable option to help refinance the loans that you took out to pay for your undergraduate or graduate education. Discover Student Loans is one of the largest providers of private student loans in the United States. In addition to student loans, Discover Bank offers a variety of banking and lending products that feature great service and benefits.

The Basics

Discover Student Loans offers many different kinds of student loans, including undergraduate loans, health professions loans, residency loans, law school loans, bar exam loans, MBA loans, graduate loans, and consolidation loans. The breadth of their student loan options makes them unique among other lenders who often just specialize in one type of loan. Their consolidation loans allow you to refinance both private and federal student loans – although you will lose many of the protections that you have on your federal loans if you refinance them.

Discover Student Loans approves consolidation loans based on credit-worthiness and consumers have the option to apply on their own or may have the option to apply with a co-signer. By applying with a creditworthy co-signer, you may receive a lower interest rate. A co-signer is usually a family member or close friend who agrees to guarantee that the loan will be repaid. Recent grads may consider requesting help from their previous co-signer when refinancing their loans. Unlike some other lenders who offer co-signer release, which allows you to remove a co-signer from the loan after a certain number of on-time payments, Discover does not offer co-signer release. That means the co-signer is responsible for the life of the loan.

Discover Student Loans offers both fixed rate and variable rate consolidation loans (which are tied to LIBOR rates). The interest rates on their student loan consolidation options are between 3.87% APR – 7.12% APR (3-Month LIBOR + 2.49% to 3-Month LIBOR + 5.74%)1 on variable rate loans and between 5.24% – 8.24% and 5.49% – 8.24% APR1 on fixed rate loans with a 10 year and 20 year repayment term, respectively.

Depending on your credit score and income or that of your co-signer, consolidating your loans with Discover could allow you to save a significant amount of money.

When it comes to term lengths, Discover consolidation loans allow you to choose between a 10 and 20-year repayment term. You’ll likely save money on interest if you choose the shorter term.

Discover Student Loans Benefits

Discover Student Loans doesn’t charge origination fees, late fees, or application fees. There are also no prepayment penalties or early repayment penalties if you want to pay off your student debt early or if you want to add a little extra to your payment every month.

Like many other student loan lenders, Discover gives borrowers a 0.25% interest rate break when you are enrolled in auto-pay for their student loans. The lowest listed APRs shown above include a 0.25% rate reduction for automatic payments2.

Finally, one big benefit of dealing with Discover Student Loans is that they have amazing customer service. The company’s Student Loan Specialists are all based in the U.S., and are available 24 hours a day. While the online application for Discover Student Loans is straightforward and only takes around 15 minutes to complete, these customer support specialists are able to help with your application or with any questions you have about your Discover loan.

To Consider

To consolidate your student loans with Discover, you must be a U.S. citizen or permanent resident with a U.S.-based address and have no more than $150,000 in total student loan debt unless you studied in a specific field which tends to have higher average debt. That means that Discover consolidation loans might not be an option for some international students or for those with significant amounts of debt.

Also, the application process is relatively easy and online with Discover and it can take from 30 to 45 days to process the loan.

Depending on your individual circumstance, Discover’s rates may be higher than some of the other companies mentioned above. The amount that you’ll pay will depend on your particular financial situation, and you might end up paying more if you take out a Discover consolidation loan. For that reason, it’s critical that you shop around before deciding where to consolidate your student loan.

Discover Student Loans have zero fees– no application, origination or late fees. That being said, Discover does not offer things like career services and job placement help or other benefits.

Discover offers reasonable rates, great customer service, and no fees. That said, are other companies that claim to offer lower rates, faster processing times, and more benefits for borrowers. Before you consider Discover to consolidate your student loans, we always recommend that you compare not just interest rates, but also company reputation and customer service.

Bottom Line

LendEDU gives Discover Student Loans our stamp of approval. Click below to see if you are eligible at Discover Student Loans!

- Refinances and issues private student loans

- 10-year or 20-year repayment terms on consolidation loans

- Variable rate loans between 3.87% and 7.12%1

- Fixed rate loans between 5.24% and 8.24%1

- 0.25% auto-pay discount included in lowest listed APRs2

- Strong credit score and salary or a co-signer may be needed

- Zero pre-payment penalty

- Zero origination fees

- Great customer service

- See Discover Student Loans Disclosures1,2

We want to be transparent. LendEDU does receive compensation from Discover in exchange for online advertisements on our website. However, the findings of our research are based on authentic and unbiased analysis of product features.

8. Earnest Review

Earnest is one of the most unique student loan refinance and consolidation lenders. Since the company’s founding in 2013, it has expanded to over 160 employees and has grown into one of the top refinancing lenders. Located in San Francisco, Earnest offers both new personal loans and student loan refinancing. Unlike most of the other companies mentioned on this page, Earnest utilizes extensive data to determine eligibility and plans for applicants who wish to refinance. This data helps them decide how likely individuals are to pay back their debt, and what the best options for all parties involved is. If you have student loans, definitely give Earnest a look.

The Basics

Earnest offers some of the the lowest interest rates in the market. Variable rates, which vary as the LIBOR changes, start at 2.82%. Fixed rates, on the other hand, stay the same throughout the life of the loan, and may be as low as 3.35%. All of these rates include a 0.25% discount for enrolling in auto-pay. These are extremely low rates and give the potential for loads of savings. In fact, the average Earnest customer saves $21,810 through refinancing. One of the most unique benefits that Earnest offers is the option to choose a repayment length of anywhere between 5 and 20 years.

Borrowers can both refinance and consolidate their educational debt through Earnest. Like SoFi and Citizens Bank, both federal and private student loans are eligible. If you choose Earnest and are approved after applying, the company will send a payment to your old provider to pay off your old loans. You will then be issued a new one with a lower interest rate or different repayment term. Finally, the company charges no application, origination, and prepayment fees.

Earnest Benefits

Earnest may have more benefits than any of the lenders. It has all of the typical benefits such as an auto-pay discount, no fees, and great customer service.

Besides those, Earnest has an extremely unique application process. The company has its and your best interests in mind when considering whether you are eligible. The company uses thousands of data points to see if you are qualified, ensuring that you will successful in repayment.

You can see a screenshot of the beginning of Earnest’s application to the right.

It has 5 sections in total, all of which require some basic information.

One benefit of Earnest that very few other lenders can claim is that it does not outsource you to a servicer. Earnest keeps all of its customers and sticks with them through the entire repayment process. The company’s Client Happiness team is available around the clock to help you out with any problems that may arise.

Possibly the best benefit of choosing Earnest is that customers have the option to temporarily defer payments in the case of financial hardship, such as in the case of job loss. In addition, those who want to return to school can defer payments for up to 3 years. You can use these student loan calculators to predict the costs of different repayment scenarios. Earnest also lets customers skip one payment a year after they have made on-time payments for 6 months, as long as they make up the missed payments with subsequent payments.

Earnest also allows users to switch between a variable and fixed rate once every 6 months after 6 months of on-time payments. Lastly, borrowers can make bi-weekly payments so less interest accrues, saving them significant amounts of money.

To Consider

Because Earnest considers many different factors to determine eligibility, there is more likely to be something on your application that causes you to be rejected. In addition, the application process is more extensive and takes a longer time due to the variety of data points that are analyzed.

Bottom Line

Earnest’s student loan refinance and consolidation program is perfect for people who want:

- To save money with a lower interest rate

- A flexible repayment plan

- A servicer who treats each customer as an individual

- Want their eligibility to be based off more than credit score

LendEDU gives Earnest our stamp of approval. Click below to see if you are eligible at Earnest!

- Refinance and consolidate both federal and private student debt

- Have completed school of are in the final semester of degree

- Have at least $5,000 in student debt

- Variable rates as low as 2.82% APR with auto-pay

- Fixed rates as low as 3.35% APR with auto-pay

- Data-driven eligibility requirements

- No application, origination, or prepayment fees

- Unique deferment options including job loss protection

- Options to switch between variable and fixed interest rates

- Bi-weekly payments

9. Laurel Road- A Division of Darien Rowayton Bank – Review

Based out of Darien, Connecticut, Laurel Road (A Division of Darien Rowayton Bank, or DRB), is known for its incredibly low rates and tight interest rate ranges. The company offers its customers a number of term lengths with variable and fixed interest rate options. Today, the company allows borrowers to refinance and consolidate both federal and private student loans together into a new one. This is great for borrowers who are stuck making multiple payments each month.

At LendEDU we work with only the top student loan refinance and student loan consolidation companies. At the end of the day, Laurel Road has some of the lowest interest rates available. Most borrowers can save by refinancing through Laurel Road.

The Basics

With so many new lenders who refinance student loans, it is tough to find the best in the industry. That’s on top of the issue of how hard it can be to figure out how to refinance student loans and how to consolidate student loans.

Navigating through the array of Google results can be difficult. It gets even harder when each lender has its own set of criteria, interest rates, and term lengths options available.

Each lender brings something unique for borrowers and you have to decide which is best for you. It is hard when so many refinance and consolidate student debt.

Laurel Road offers variable interest rates ranging from 3.76% to 6.42%. Alternatively, if you prefer a fixed rate, you can expect to land somewhere between 4.20% and 7.20%.

Laurel Road charges NO origination fees, a benefit that can help borrowers save money! As far as credit criteria goes, Laurel Road requires borrowers to have an excellent credit profile and good income.

Laurel Road evaluates each applicant on an individual basis so it is worth applying even if you are afraid you won’t qualify. To improve your chances of approval we suggest you apply with a cosigner.

You can get an idea of what Laurel Road’s application process looks like to the right. It is very straightforward and easy to complete. Additionally, it doesn’t take long and you can find out if you are eligible relatively quickly.

Laurel Road offers term lengths of 5, 7, 10, 15, and 20 years. The company offers both variable and fixed interest rate options. Also, there is no penalty for paying off your loan early. Borrowers are expected to make payments on a monthly basis. The company offers an interest rate discount of 25 basis points if you sign up for auto-pay.

Laurel Road Consolidation Benefits

Laurel Road offers borrowers 10 great options to refinance and consolidate student loans. Out of all the student loan refinance and consolidation lenders on the market, Laurel Road offers borrowers the most options. We are sure that every borrower will be able to find an option that meets their financial objectives.

Laurel Road has zero origination fees! Origination fees are charged to borrowers for taking out a loan. Usually, origination fees are quoted as a percentage of the loan amount. These fees are added to the principal balance. But with Laurel Road you can avoid these costs all together. By not having an origination fees, Laurel Road makes it easy to compare the value of a consolidated loan against the current loans that the borrower already has. Laurel Road has zero prepayment penalties! For those working to pay off their obligations quickly, zero prepayment penalties are important. That being said paying off your student loans early may not be a primary goal for some borrowers.

To Consider

In general, Laurel Road looks for applicants with very strong incomes and low debt. To be approved by Laurel Road you must have good credit, a well paying job, and be able to keep your debt load low. Having a cosigner can greatly improve you chances of being approved.

Bottom Line

The Laurel Road student loan refinance and consolidation program is a great option for people who want:

- To lower their monthly payment

- Lock in low interest rates

- Choose from a variety of term lengths

- Consolidate federal and private student debt

At LendEDU, we give Laurel Road our stamp of approval. To get started you can start the application at Laurel Road!

- Refinancing and consolidation for graduate and undergraduate, private and federal college debt.

- Must have achieved a Bachelors or Graduate degree.

- PLUS loans have become an extremely popular options for parents with college students. Laurel Road allows parents of degree holders to get lower interest rates on PLUS loans after the child is working and has received their degree. The parent can choose to apply in their name, or their child’s name.

- 5, 7, 10, 15, 20 year repayment terms

- Moderate credit score, salary, and debt-to-income requirements

- No origination fees

- No prepayment penalties

- 0.25% Interest Rate Reduction with automatic payments via ACH. Please note, the automatic payments are a free service for borrowers.

Education Success Loans Review

Finding the best college debt consolidation company can be tough. Each lender has its own set of criteria, interest rates, and term lengths. Moreover, each lender brings something unique for borrowers. Cosigner requirements, credit score minimums, and customer service can vary at each lender. At LendEDU we work with only the top student debt financing and consolidation companies.

One company trying working to help borrowers is Education Success Loans! Read below to learn more about how Education Success Loans can help you figure out how to refinance student loans and how to consolidate student loans.

The Basics

The lowest interest rate that Education Success Loans currently offers is 4.99% at a mixed rate. What is a mixed rate? A mixed interest rate starts at fixed, then adjusts to variable later on. Mixed rates are great for borrowers who want to lock in low interest rates today and believe that interest rates will stay low in the future. The highest interest rate offered is 7.99%.

Today, Education Success Loans allows borrowers to refinance and consolidate both federal and private student debt.

If you are a borrower stuck paying high interest rates on old federal and private student debt, Education Success Loans is a great option. The company charges NO origination fees which can help borrowers save money from the beginning.

As far as credit criteria goes, Education Success Loans requires borrowers to have a good credit score and an average debt-to-income. The company has good approval ratings, so definitely apply even if you may think you are not qualified. Many borrowers have told us that Education Success Loans approved them even with only decent credit. The lender works with each borrower on a case-by-case basis to determine eligibility and approval. Education Success Loans offers a term length of 25 years.

There is no penalty for paying off your debt early, and borrowers can pay as much as they would like each month on top of their minimum monthly payment. Borrowers are expected to make payments on a monthly basis. The company offers an interest rate discount of 25 basis points if you sign up for auto-pay. Auto-pay is easy to setup and convenient for borrowers. No longer will you need to worry about sending in checks to pay for your student loans.

Education Success Loans Benefits

Education Success Loans offers borrowers three great options to refinance and consolidate student loans. Out of all the student loan refinance and student loan consolidation lenders on the market, Education Success Loans is one of the only lenders to offer 25 year term lengths. If you are looking to lower your monthly payment, you can bet that a 25 year term will do the trick. By spreading your repayment out of 25 years you will be required to pay much less each month.

Education Success Loans has zero origination fees! Origination fees are fees charged to borrowers for taking out a loan. Usually, origination fees are quoted as a percentage of the balance. These fees are added to the principal of the loan. But with Education Success Loans you can avoid these costs all together. By not having origination fees, it is easy to compare the value of a consolidated loan against the current loans that the borrower already has.

Education Success Loans has zero prepayment penalties! For people working to pay off their student debt quickly, zero prepayment penalties are important. Some lenders charge borrowers when they pay off their loans early. So if you come into that year end bonus, you don’t need to fear paying off your loans early. You may be fearful to extend your student loans out to 25 years, but with zero prepayment penalties you can easily pay off your student loans early if you so choose.

To Consider

The biggest disadvantage of Education Success is that they are a smaller lender in the industry. As a result, the company has only one 25 year term length available for borrowers. That being said, you can choose to pay back your funds without a prepayment penalty if you would like. The other disadvantage is that Education Success only offers mixed interest rates. This could be an issue for some borrowers looking to lock in low interest rates today. If you are worried that interest rates will rise in the short term, you should select an option with a fixed interest rate.

Bottom Line

The Education Success college debt refinancing and consolidation program is a great option for people who want:

- To lower their monthly payments

- Zero prepayment penalties

- A longer 25 year term length

- Consolidate federal and private college debt

- Want a personalized customer service experience

At LendEDU, we give Education Success our stamp of approval. To get started you can start the application at Education Success!

- Private student loan consolidation for private and federal student debt

- 25 Year Repayment Term

- 1 Year Fixed 4.99% then variable rate for the remaining term

- 5 Year Fixed 5.99% then variable rate for the remaining term

- 10 Year Fixed 7.99% then variable rate for the remaining term

- Auto-Pay: 0.25% Interest Rate Reduction with automatic payments via ACH

- No Origination Fees

- No Prepayment Penalties

- Must have graduated at least 30 months prior to application date

- Have a minimum of $5,000 ($15,001 if in Kentucky) in student debt

- Supply acceptable proof of income of at least $24,000 annually

- Be a US Citizen or Permanent Resident and continue to be a Permanent resident of DC or any state in the continental United States other than AZ, IA, IL or WI

iHelp Loans Review

iHelp Student Loans is a smaller student loan organization working to help graduates best manage their debt. iHelp recently launched a student loan consolidation service in partnership with its lender partners. iHelp is a middleman of sorts. In short, iHelp matches student debt borrowers with smaller and community banks. Community banks, like credit unions, usually focus in on one particular geographical area. Community banks are eager to help customers manage their student obligations. With iHelp’s undergraduate Loan Consolidation program more community banks can get into the undergraduate loan market.

At LendEDU, we like to work with as many lenders as possible. Why? Well the more lenders we have on our college debt refinancing platform the better. Community banks are known to offer some great interest rates and even better customer service. Keep reading below to figure out how to consolidate student loans and how to refinance student loans with iHelp.

The Basics

iHelp offers competitive student debt refinancing and consolidation rates and terms to prospective borrowers. The company has two different rates depending on if you apply with or without a cosigner. If you apply with a cosigner, rates start at 6.00%, or 6.22% APR. If you apply without a cosigner, your starting rate could be as low as 7.00%, or 7.21% APR. All of iHelp’s consolidation rates are fixed rates. Meaning, all of the interest rates will not change over the life of the loan. Your monthly payment and total cost will not change with iHelp’s student loan consolidation program.

iHelp does charge its borrowers a supplemental fee at the time of disbursement. iHelp charges 2% on top of the balance as a fee for processing the new student loan. Most lenders these days do not charge disbursement fees. iHelp is unique in this area.

iHelp only allows borrowers from only certain schools to apply for its program to consolidate student debt. The approved school list is fairly large. Know that the participating schools are in the following states: California, Connecticut, Delaware, Illinois, Maryland, Michigan, Minnesota, Missouri, New Jersey, New York, Ohio, Pennsylvania, Rhode Island, Virginia, West Virginia, and Wisconsin.

The reason that iHelp only allows certain schools is that the community bank partners tend to only focus on certain geographical regions.

In order to qualify you must be creditworthy. According to iHelp’s website, creditworthy means:

-

Has not had open collections or charge offs in the past 2 years.

-

Does not have bankruptcies, foreclosures, or repossessions during the past 5 years.

-

Has not defaulted on a federal or private undergraduate loans.

-

Meets the minimum credit score.

-

Has at least 2 years of credit history.

-

The borrower or cosigner must have an annual income of $24,000 or greater for the past 2 years to qualify for the iHELP Consolidation Fixed Rate Program.

-

Does not exceed the debt to income threshold of 45%.

You should know that additional credit criteria may apply.

iHelp’s consolidation loan is administered by the Student Loan Finance Corporation (SLFC) and sponsored by the Independent Community Bankers of America (ICBA). Loans are funded by an iHELP originating lender.

iHelp Benefits

iHelp offers a number of benefits to its student loan consolidation customers.

Our favorite benefit offered by iHelp is its cosigner release benefit. Having a creditworthy cosigner can really help you get approved for the iHelp consolidation program. After 24 month, you have the ability to release your cosigner from the loan. You must have made all 24 monthly payments on time to do this. You must also meet iHelp’s credit requirements in order to qualify for cosigner release. Even so, cosigner release is an awesome benefit to offer!

If you refinance with iHelp, you will have the choice of three different repayment options. Of course you can just choose the standard repayment, but there are a couple unique options to consider. iHelp offers interest-only payments. Meaning, the borrowers has the option to pay only interest for 24 months. This is a great option for borrowers looking to temporarily lower their monthly payment. iHelp also offers graduated repayment. This option allows borrowers to make interest-only payments for a set period of time and then gradually overtime the payment amount increases until the borrower is making the full principal and interest payments.

iHelp even offers forbearance options to borrowers. If you fall into a financial rut, iHelp has your back and can help you delay your monthly payments with forbearance.

To Consider

If you are a very qualified candidate for student debt consolidation, iHelp is probably not your best option. iHelp’s student loan consolidation interest rates tend to be a little high. If you are a very qualified candidate, you can probably get lower interest rates at another one of the refinance lenders.

Moreover, the supplemental fee charge by iHelp is expensive. The supplement fee is currently set at 2% of the balance. You need to factor in the costs of the supplement fee when considering iHelp’s interest rates. The APR rate will include the supplemental fee.

The Bottom Line

The iHelp Student Loan Consolidation program is a good option for some borrowers who:

- Want to consolidate college debt

- Are interested in cosigner release

- Want interest only payment plans

- Want a community bank lender

At LendEDU, we give iHelp a stamp of approval. Check out their website for more information and to get started.

- Rates start at 6.00%, or 6.22% APR

- 15 year term length

- Only fixed rate options

- Cosigner release is available after 24 months

- Interest only payments are available for 24 months

- Graduated payments available

- Community bank lenders

- School must be on accepted school list

Federal Direct Student Loan Consolidation

Are you trying to figure out how to consolidate student loans with the government, not with a private lender? Then you have come to the right place. Keep reading below to learn more about federal consolidation.

You can, in fact, consolidate federal student loans without a new private lender. The Department of Education allows you to consolidate federal student loans through the Direct Consolidation Loan program. The Direct Student Loan Consolidation program allows you to consolidate federal student loans into one new loan. It does not allow you to refinance student debt.

You will not need to pay any fees to consolidate federal student debt through this program. You can consolidate your federal student loans for free online. Do not pay for consolidation!

When you take out a Direct Consolidation Loan, you replace multiple federal student loans with one, requiring only one payment per month. To qualify, you must have one or more federal loans (Direct or FFEL) that are in repayment or in a grace period. These are the types of federal student loans that can be consolidated:

- Direct PLUS

- Direct Subsidized

- Direct Unsubsidized

- Federal Nursing

- Federal Perkins

- Health Education Assistance Loans

- PLUS loans from the Federal Family Education Loan (FFEL) Program

- Subsidized Federal Stafford

- Supplemental Loans for Students (SLS)

- Unsubsidized Federal Stafford

In addition, some existing consolidation loans can be reconsolidated if you include an additional Direct or FFEL loan, although you may be able to reconsolidate an FFEL loan without including other loans.

Not only does student debt consolidation simplify your monthly repayment schedule, it can reduce your monthly payments by extending your repayment period to 30 years. You also might gain access to alternative repayment plans and/or replace variable-rate loans with a fixed-rate loan. These repayment plans include options to pay less now and more later, to base payments on earnings, or to cap payments as a percentage of discretionary or annual income:

1. Standard: You have up to 30 years to repay a standard consolidation loan. All federal borrowers are eligible for this.

2. Graduated: Payments start off low and increase over time, usually in steps every two years.

3. Pay As You Earn: The limit on monthly payments is 10% of discretionary income. Your payments are recalculated annually based on your family size and income. Family income is included if you file a joint return. You receive forgiveness on any balance remaining after 20 years (beware that forgiven debt may be taxable). This plan is available to loans taken out after September 30, 2007, and you must have a high debt-to-income ratio.

4. Revised Pay As Your Earn: Family income and amount of debt are considered independent of how you file your tax returns. Also, forgiveness starts after 20 or 25 years.

5. Income-Based: Payments will be 10% or 15% of discretionary income. Otherwise, this resembles revised pay as you earn.

6. Income-Contingent: Available for student and parent loans. You pay the lesser of:

a. What you would pay on a 12-year, income-based plan

b. 20% of your discretionary income

7. Income-Sensitive: Annual income determines your monthly payments. These can have terms of up to 15 years.

How to Consolidate Student Loans through the Government

You can apply for a Direct Consolidation Loan after you leave school, drop below half-time enrollment, or graduate. However, you cannot consolidate student debt on a defaulted loan unless you first make arrangements with the current servicer, or you agree to repay the consolidated loan under one of the income-driven plans. There are no application or prepayment fees for this.

The Federal Student Loan website allows you to apply for a Direct Consolidation Loan electronically or with paper forms. You can apply online by first choosing the existing loans, then picking one of the many repayment plans. You then sign the application after you review all the terms and conditions. The servicer will arrange to pay off your existing debt and set up your consolidated repayments.

Normally, repayment of a Direct Consolidation Loan commences within 60 days of disbursement. If your existing debt is still in its grace period, you may be able to delay repayment until your grace-period end date. Your repayment period will be 10 to 30 years, depending on several factors.

Pros and Cons

Pros:

1. Simplifies and centralizes your repayment schedule

2. Offers the opportunity to reduce your monthly payments

3. Offers the opportunity to adopt an income-driven repayment plan

4. Converts variable rates to fixed rates

Cons:

1. May increase the number of payments and interest paid

2. Does not include private and parent student loans

3. May lose certain existing benefits

4. Interest rate is not lowered

5. Does not save money like refinancing and consolidating through a private lender

Avoiding Consolidation Loan Scams

Consolidating multiple federal student loans is a good idea after you graduate. However, you must be vigilant when it comes to consolidation scams. The most popular scam involves companies charging you a fee, sometimes as high as $1,000, to consolidate your loans. Remember, consolidation is free and you can accomplish it at the Federal Student Aid website.

Another scam is one in which a company offers you “immediate debt relief,” implying a cut in your principal balance or interest rate. Instead, the company charges a hefty fee and, at best, puts in the paperwork to consolidate your loans. At worst, they take your money and do nothing. As an example, the Consumer Financial Protection Bureau shut down College Education Services in 2014 because it was running illegal debt relief services.

Look for these red flags before considering the use of a private company for federal student loan consolidation:

- Pressure tactics: It is illegal to demand upfront fees for consolidation assistance. Beware if they ask you to sign some sort of contract or to reveal your credit card/bank account number.

- Immediate relief: No company can truthfully promise to immediately reduce or cancel your debt. If a company tells you it can work out a special deal with the DOE, consider reporting it to the authorities. Debt relief is only possible via the approved federal student loan programs.

- Third party authorization: Any company asking you to sign a third-party-authorization or power-of-attorney document is probably crooked. There is no reason to grant these companies any of your rights, nor should you make your repayments through them.

- Stealing your PIN: Your Federal Student Aid PIN uniquely and secretly identifies you to the DOE for matters relating to federal student loans. If a company asks for your PIN, it’s equivalent to stealing your signature. Honest companies will never ask for your PIN.

If you wish to submit a complaint about a company offering student debt relief services, call the CFPB at (855) 411-2372 or file a complaint online.

If you have questions about federal student loan consolidation, you can contact the Loan Consolidation Information Center at 1-800-557-7392. LendEDU does not represent the Department of Education in any way. Please consult a financial adviser before consolidating federal student loans.

Differences Between Federal Consolidation and Private Consolidation

|

Federal |

Private |

|

|---|---|---|

|

May Receive Lower Interest Rate |

No |

Yes |

|

May Save Money |

No |

Yes |

|

Keep Federal Benefits |

Yes |

No |

|

Federal Loans Eligible |

Yes |

Yes |

|

Private Loans Eligible |

No |

Yes |

Please note: Your ability to receive a lower interest rate or save money varies depending upon your starting interest rate, starting terms, and other factors.

If you have student loans, you may be have heard about consolidation or refinancing as a method to combine many loans into one, potentially reducing your interest rate or monthly payment. These terms are often used interchangeably, but have different goals and are utilized for different reasons.

Consolidation is generally used to combine many loans into one. It can be used for federal student debt through federal consolidation, or private and/or federal student loans through private refinancing and consolidation. When you refinance multiple student loans, including both private and/or federal student loans, you are effectively consolidating them because you will be combining all of them into one new loan.

Federal Consolidation vs. Private Refinancing

Refinancing and consolidating with a private lender results in an entirely new interest rate, which is often lower than the original rate or rates. This is typically the goal of refinancing: to obtain a lower interest rate based on your credit score, income, history of on-time payments, and other factors. With federal consolidation, the rate for your new loan that you receive is based on a weighted average of your old loans’ rates, rather than an entirely new interest rate. With consolidation, you can typically extend your repayment schedule to up to thirty years. Refinancing payment terms are generally anywhere from five to twenty-five years.

Pros & Cons of Each

There are advantages and disadvantages to both refinancing and consolidation. With refinancing, you can often save money by obtaining a lower fixed interest rate for your student debt. You can also often lower your monthly payment and shorten your repayment term, enabling you to pay off your debt sooner and allowing you to save money on the total amount of interest that you pay. However, if you refinance both federal and private student debt together — which is essentially a form of private consolidation — you lose the protections of federal student loans, which may be useful for some borrowers. This includes income-based repayment plans, student loan forgiveness options, and other benefits that are only available to borrowers with federal student debt.

Federal loan consolidation offers borrowers a way of simplifying their finances by giving them just one bill to pay each month for their federal student loans. If you have an older (pre-2006) variable rate federal student loan, consolidation can save you money by allowing you to take advantage of fixed interest rate terms. Consolidation may also lower your monthly payments through extending the loan repayment term, but be aware that a longer loan term results in spending more over the life of the loan due to more interest payments. Federal loan consolidation also does not save you money; it is typically done more for convenience than to lower payments or interest rates. There is currently no way to reduce the interest rates on federal student debt without switching to a private lender.

Consolidating Parent PLUS Loans

Parents of dependent undergraduate students can receive a federal Direct Parent PLUS Loan if parent and child both meet the general eligibility requirements. The obligation to repay the loan rests solely with the parent, and the DOE doesn’t permit the direct transfer from parent to child. However, there is a work-around: The child can apply to a participating private bank or company to refinance in the child’s name.

Several student loan refinancing companies, including SoFi, Laurel Road (A Division of Darien Rowayton Bank), and CommonBond offer this option to children whose parents took out a Direct Parent PLUS Loan. Generally, the child must have graduated with at least a Bachelor’s degree and be professionally employed.

Each refinance company evaluates the child’s application using its own criteria, but generally, the lenders want to be sure that the child can repay the loan. Typically, this requires the child to provide information about financial history, career experience, the school attended, the kind of degree received, and current income and expenses.

How to Choose Which is Right for You

Deciding whether to consolidate or refinance your student debt depends on your specific situation. If you currently have high interest rates or a variable rate loan, you may want to consider refinancing your student loans. However, if you depend on income-based repayment plans or intend to apply for forgiveness through the federal government, then refinancing may not be a smart choice for you. If you are considering refinancing or consolidating your student loans, carefully review the terms of your loans. Take advantage of online refinance calculators to determine whether you would save money with a lower interest rate, and be sure to comparison shop for the best rates.

Student Loan Refinancing & Consolidation Application Process

If you have decided to refinance your student loans, congratulations on taking control of your financial future! For many borrowers, refinancing is a tool that can save substantial money, both in monthly payments and over the life of a loan. Here are the general steps to the student loan refinancing application process:

- Do your research to see if refinancing is for you

- Compare options using LendEDU’s application for free (optional)

- Choose lender to apply to

- Fill out basic background & education information

- Upload required documents

- See if you are prequalified

- Wait for full approval/denial from lender

When you apply for a student loan refinancing, it is like applying for a new loan. The bank or lender will look at your credit score, income, the amount of savings you have, your educational background, and the number of on-time payments that you have made so far with your student loans. Generally, your credit score must be no lower than the mid-600’s (660 or higher) to qualify, or you may need a co-signer. Each lender will have different specific requirements, such whether or not you can still be in school when you apply, the maximum and minimum balance that you can have in order to refinance, and the number of on-time payments you must make before you can apply to refinance your loan.

To start the process, you should gather information about your student debt. If you do not have a copy of your student loan documents, you can get them in one of two ways. For federal student loans, you can view them directly online at the Federal Student Aid portal or the National Student Loan Data System. You will need to log in using the PIN number that you used to apply for student aid. Private student loans can be found via your credit report. You are entitled to a free annual copy of your credit report, which can be obtained from one of the major credit reporting agencies. Once you have determined which loan companies hold your loans, you can get a copy of your loan documents directly from those companies.

Once you have all of the information about your student loans, carefully consider your refinancing options. LendEDU allows borrowers to compare a number of lenders, providing information such as rates, whether the rates are variable or fixed, terms, loan types, and ranking. This level of transparency empowers borrowers to make the best possible decision when it comes to refinancing their student debt. Rates for these loans range from as low as 2.39% to 12%.

If you decide to apply for a loan through a bank or other lender, the lender will review your application and if you are approved, will decide your interest rate based on the factors discussed above. Your new servicing company will then pay off all of your old student loans, and you will receive statements from the new lender each month. Instead of receiving multiple statements and paying multiple bills, you will have one payment each month.

With LendEDU’s simple online comparison tool, refinancing federal and private student loans is a simple, straightforward process that can help save you money.

How Cosigners Affect Refinancing & Consolidating Student Loans

Benefits of Using a Creditworthy Cosigner:

- More likely to be approved

- Receive a lower interest rate

- Have someone to motivate you to stay on top of loans

- Cosigner may be discharged after certain number of on-time payments

Risks of Using a Cosigner:

- Credit of primary borrower and cosigner will both be affected if payments are missed

- Cosigner’s retirement could be delayed

- Cosigner will be required to make payments if primary borrower does not

When it comes to paying for college, many borrowers are turning to private student loans to close the gap between savings, student aid, scholarships, grants, and federal student loans. In many cases, lenders require borrowers under the age of 25 to have a cosigner in order to be approved.

The cosigner requirement enables many students to borrow money for college or graduate school who otherwise would not qualify for student loans on their own, but it can be a significant burden for family members or friends who serve as cosigners. Like new private student loans, borrowers looking to refinance can benefit by adding a cosigner.

Who Can Cosign?

A cosigner is a person who assumes equal responsibility for a student loan. If the primary borrower either does not repay the loan or goes into default, the co-signer becomes responsible for the loan. In some cases, the entire amount of the student loan may be due immediately if the primary borrower goes into default. Otherwise, the cosigner may be required to take over the monthly payments on behalf of the borrower.

Why Use a Cosigner?

The rationale behind cosigners is that in most situations, the primary borrower is young, and probably will not have much credit history. Private student lenders and refinance lenders cannot evaluate their credit risk because the borrowers may not have a track record of paying bills on time, or borrowing money and repaying it. There is no way for lenders to know if these applicants are a good credit risk. For this reason, they are reluctant to lend large sums of money or refinance large sums of money without a guarantee that someone will be responsible in the event that the primary borrower will be unable to pay the debt.

A cosigner with a credit history and a higher credit score can help a borrower be approved for student loan refinancing and consolidation, and can also assist in obtaining a lower interest rate. This is because the lender knows that if the primary borrower is unwilling or unable to pay back the student loan, the cosigner will be required to assume the payments. The interest rate for a refinanced loan may drop by over 2% simply by having a cosigner. The lender knows that a cosigner with a strong credit history is a good credit risk and will be more likely to pay back the loan than the primary borrower without any credit history.

What are the Risks of Cosigning?

Of course, there are some drawbacks to being a cosigner for a refinanced student loan. If something happens to the primary borrower — including death, disability, unemployment, or simple financial irresponsibility — then the cosigner will be required to pay back the loan. As a co-signer you will be required to pay back to loan if the primary borrower fails to do so, regardless of the reason for his or her failure. Late payments or missed payments can also negatively impact your credit score. Carefully consider the wisdom of cosigning a refinanced loan before agreeing to sign on behalf of a child, grandchild, other family member or friend.

Can Cosigners Ever be Released from the Loans?

There is a method by which cosigners can be let off the hook after certain conditions are met. Once a student has graduated from college or graduate school and has started making regular, on-time payments, the cosigner may be able to obtain a release when refinancing. Most lenders have a program that permits borrowers to reapply for refinancing under their own names only, releasing the cosigners from responsibility. As long as the primary borrower can demonstrate that he or she is capable of repayment without the cosigner, then the cosigner will be released from responsibility. Check with your lender to determine if there is a cosigner release program through refinancing, and what the terms of the program are.

How Refinancing Interest Rates Work

Student loan refinance rates can be as low as 2.39%. Refinancing to lower rates can save some borrowers upwards of $20,000 over the life of their loan! Also, you can consolidate multiple student loans into one when refinancing.

Over the last couple years student loan refinancing and consolidation has become a hot topic in the United States. As it sounds, refinancing allows undergraduate and graduate borrowers to refinance student debt at a potentially lower interest rate.

That being said, not all student loans are created equal. Interest rates usually vary by loan type, rate type, and credit worthiness. If you find yourself paying 4% to 10% in interest each year, you are paying too much.

Refinancing can be a smart choice as a way to lower your interest rate or to change your interest rate from variable to fixed. But in order to understand whether or not refinancing is a good option, you first need to understand the basics of how refinancing interest rates work.

Current Student Loan Refinancing Interest Rates

Variable Rates

2.39% – 8.38%

Fixed Rates

3.25% – 8.24%

How Interest Rates Work in General

Interest rates are the amount that a lender charges a borrower for the use of money, typically expressed as a percentage of the total amount borrowed. For example, if you borrowed $10,000, and the interest rate was 10%, then you would pay $1,000 to the lender for the use of that money. Typically, interest rates are charged on a yearly basis, which is known as an annual percentage rate, or APR. Over the life of a loan, interest rates can represent a substantial amount of money. In the $10,000 example above, in a 5 year term, the total interest paid would be $2,748.23 — or nearly one-third of the total amount of money borrowed.

Student Loan Refinancing Interest Rate Information